Circana’s Rory Partis looks at whether the sluggish start to the festive season should be a cause for alarm or whether we should be hopeful that consumers are looking to spend late.

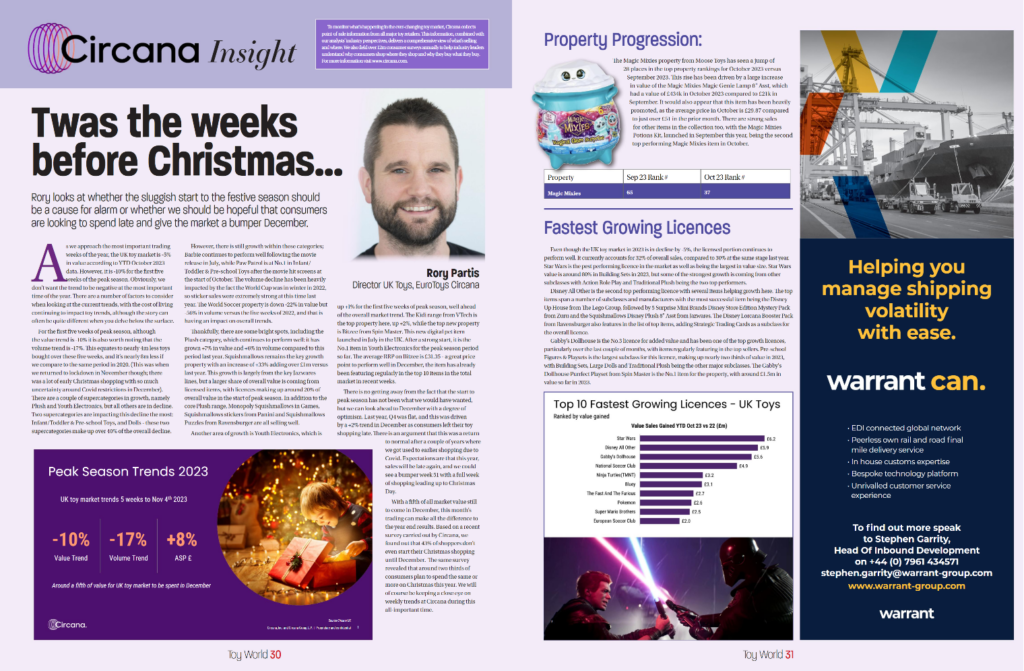

As we approach the most important trading weeks of the year, the UK toy market is -5% in value according to YTD October 2023 data. However, it is -10% for the first five weeks of the peak season. Obviously, we don’t want the trend to be negative at the most important time of the year.

There are a number of factors to consider when looking at the current trends, with the cost of living continuing to impact toy trends, although the story can often be quite different when you delve below the surface. For the first five weeks of peak season, although the value trend is -10% it is also worth noting that the volume trend is -17%. This equates to nearly 4m less toys bought over these five weeks, and it’s nearly 8m less if we compare to the same period in 2020. (This was when we returned to lockdown in November though; there was a lot of early Christmas shopping with so much uncertainty around Covid restrictions in December).

There are a couple of supercategories in growth, namely Plush and Youth Electronics, but all others are in decline. Two supercategories are impacting this decline the most: Infant/Toddler & Pre-school Toys, and Dolls – these two supercategories make up over 40% of the overall decline.

To read plenty more about current growth areas, property progression and fast growing licences, click here for the full Circana insights.